Will the euro zone get stuck in a long period of stagnation? The question is worth exploring at a point where growth is at a standstill in Germany and Italy, while the euro zone as a whole has seen growth drop to under 1%...despite an all-time accommodative monetary policy.

If an economic shock were to hit tomorrow, Europe would have nowhere left to turn. The ECB has already done a lot. Its rates are in negative territory, and its policy is having less and less of an impact on economic activity, whereas the side effects are becoming increasingly clear: by driving real estate and financial prices up, the central bank has taken the risk of seeing bubbles gradually take shape. By hurting the bottom line of insurers and banks alike, it has also weakened the financial system. As for turning to the other pillar of economic policy, i.e. fiscal policy, this particular tool is practically no longer used to stimulate activity: many countries are struggling with high public debt, and the TSCG (Treaty on Stability, Coordination and Governance) signed in 2012 prohibits EU Member States with debt exceeding 60% of GDP from indebting themselves even further. So, unless the treaty is revoked, that avenue basically leads to a dead end...especially since the few countries that do have some wiggle room left are hesitant to use it! Germany, in particular, strongly influenced by ordoliberalism, still sees no emergency, nor even the need for fiscal stimulus. With an unemployment rate barely above 3%, it’s true that its economy is very close to full employment.

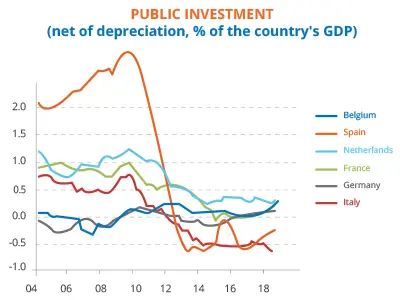

So is Europe really doomed to stagnation? Granted, the central bank has few tricks left up its sleeve to drive activity, although newly arrived President Christine Lagarde has stated “there's a bottom to everything, but we're not at that bottom at this point in time.” When it comes to fiscal policy, however, the boundaries are less obvious. In the past Europe has always been able to find room for manoeuvre when needed. As it happens, the need is more urgent than it might appear at first glance. First, because a stagnant economy is a vulnerable economy: any little shock can easily tip it over into recession. Next, because, until Europe has found its way back to sustainable growth, it will have a hard time regaining the support of the people. And, finally, because the euro zone is facing a serious investment deficit: since the early 2000s, capital expenditures have grown three times slower than in the United States and, in the last two decades, government investment net of amortisation has not grown at all!

The new European Commission has a considerable weight on its shoulders. President Ursula von der Leyen has given herself 100 days to put in place a green deal to make Europe “the first climate-neutral continent” by 2050. To that end, she proposes to turn part of the European Investment Bank (EIB) into a Climate Bank and launch a “Sustainable Europe Investment Plan” aimed at raising €1,000 billion during the 2020s. A commendable plan, but it will never happen unless it’s approved by all EU national governments. What’s more, the goal is much less ambitious than it appears. The blueprint is drawn from the Juncker Plan, established in the wake of the sovereign debt crisis. Meant to get the European economy back on its feet, in the last five years it has been funded by just €26 billion in guarantees, taken from the European budget, and only €7.5 billion in capital, contributed by the EIB (i.e. less than 0.1 euro zone GDP point per year!). Furthermore, it isn’t clear that the projects financed by the Juncker plan wouldn’t have been implemented regardless.

The euro zone is currently in a paradoxical situation. Contrary to popular belief, it is not at all living above its means. Just look at its current account surplus for proof: taken altogether, its economic agents (households, corporations and governments) are still spending nearly €400 billion per year less than they earn! However, its self-imposed rules prevent the euro zone from putting that money to work to generate growth. It’s ultimately up to the Member States to assume their responsibilities, together, and invest to prepare for the future.