Equity markets keep going up. Risky assets are supported by expectations of new stimuli in the US and elsewhere. The vaccine rollout is ahead in the UK, the US and Israel, with more than 30% of the population having received the first jab. In spite of renewed short-term lockdowns, most economies are still expanding. As the recovery continues, the reflation trade has further room to grow. However, the coming weeks will oppose the risk of disappointment regarding the efficacy of the vaccines with the new variants – and there are a few – and the risk of overheating in the United States in H2. We are hence keeping some protections.

Reflation trade has room to grow

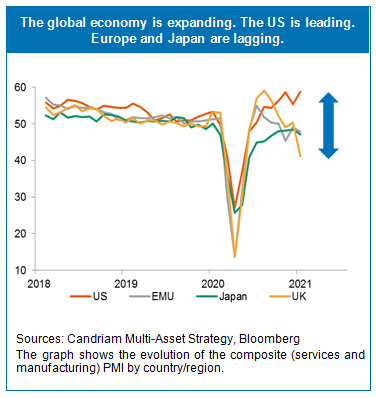

Given the current context, we believe that the reflation trade has room to grow. Economic growth is accelerating, albeit with slightly less dynamism. Some countries have had to renew with short-term lockdowns and, although these are weighing on activity, most countries are in expansion. The UK is going through a slower patch but that was to be expected.

Meanwhile, the US is in a leadership position in terms of growth, both structural and cyclical. Further, in the US, too, additional fiscal policy easing is expected. President Joe Biden has set the bar high, with a substantial proposal of USD 1.9 trillion. The current enhanced unemployment benefits of $300 a week are available to all workers in receipt of unemployment benefits, like the prior $600 weekly supplement provided by the CARES Act, which lapsed last July. As the current boost will expire mid-March, the clock is ticking for the president, who has declared that defeating the virus and fixing the economy are his top priorities. The only source of concern, at least for small and mid-capitalizations, is the likely increase in corporate tax.

In Europe, Italy´s president has asked Mario Draghi, economist and former head of the European Central Bank (ECB), to find a majority in parliament, as Draghi may very well become Italy´s next Prime Minister. The former governing coalition, headed by the resigning Giuseppe Conte, collapsed amid disagreements over how to spend the COVID recovery money from Brussels, following which the country was plunged into crisis.

In China, the Year of the Ox starts on 12 February. Some Northern provinces are again going through lockdowns, as the virus has re-surged.

In a nutshell, the recovery is, without exception, on its way and at divergent speeds, depending on the region. The context is also highly supportive of a continuation of the rotation towards value stocks, rising rates and commodity prices. Financial conditions, of both the ECB and the Fed, are highly accommodating and the forward guidance is seen as strong. The impact on financial markets: rising equities, rising rates, a return of growth and a comeback of inflation anticipation, more so on US treasury bills than the German Bund.

One virus, several variants

The main challenge for the markets remains the extent to which the vaccines can cope with the development of new variants. The coronavirus, like other viruses, changes through mutation, and new variants occur, globally, over time. Multiple variants of the virus that causes COVID-19 have been documented during this pandemic, including in the US, the UK, Brazil and South Africa. The current vaccines were designed around earlier versions of coronavirus, but scientists believe these vaccines should still work against the new ones, although perhaps not quite as well. Early results suggest that the newly found vaccines, although offering protection against the new variants, are slightly less effective.

This means that the race against time between the vaccine rollout and the acceleration of the epidemic is still on, and presents a higher hurdle to herd immunity. The news was rather well absorbed by financial markets, with sentiment indicators turning very quickly. Down at the end of January, they were up again early February, with a spike in volatility. This did not deter investments. In fact, investment positioning and various in- and outflow analyses showed that there is room for further positive inflows in equities – particularly in Europe. Assuming a decline in volatility, a new wave of investment could be triggered.

The post-COVID world

From the largest entities to the smallest groups of individuals – and including governments, central banks, corporations, whole business sectors, and families – no one has been left unchallenged by the coronavirus and its variants.. There is no doubt that this sanitary crisis will have long-lasting effects on all.

With respect to companies and countries, the gap between relative “winners” and “losers” has widened, with some proving more resilient than others in adapting to, and coping with, the challenges brought by the virus.

In terms of regional resilience, and within Europe, there is a growth gap between Germany and countries that have managed the sanitary crisis better than France, Spain and Italy (tourist destinations where more small and mid-capitalizations are lagging) – due either to their governance or to intrinsic pre-crisis weaknesses. Within Emerging markets, China stands out compared to its peers.

The sanitary crisis has also reshaped patterns of consumption. Demand in current and post-“COVID World” sectors has increased sharply in the short term and will remain for years to come. For us, technology, on-line distribution, government spending and health are all winners.

We also identify sustainability as a winning theme in, among others, all the sectors and companies that will benefit from structurally rising government expenditures as greater attention is paid to social and environmental aspects. In Europe, the “Green Deal” climate change and the circular economy are all goof examples. Opportunities in the US are worth exploring, especially now that President Joe Biden has signed an executive order taking the US back into the Paris climate accord. Nearly every country in the world has signed up to the Paris Agreement, a landmark non-binding accord among nations to reduce their carbon emissions.

Our current multi-asset strategy

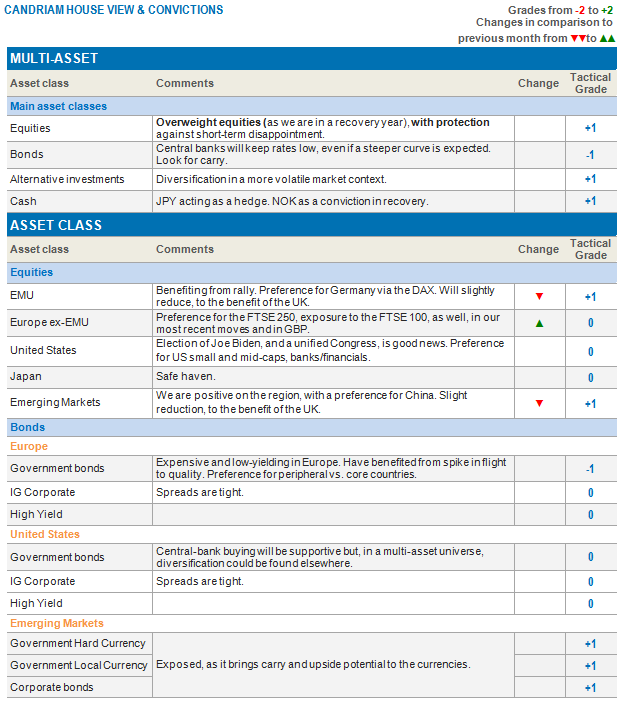

In our multi-strategy, those convictions and reflections translate into a preference for equities vs. bonds.

Within equities, our portfolio is geared towards reflation trades. We are overweight European and emerging equities, neutral US equities and overweight US smaller and mid-capitalizations. We are also overweight UK small and mid-caps, and global banks. Most recently, we decided to add to our UK equity exposure in GBP.

Within bonds, we are focusing on the carry, meaning that we are overweight emerging debt, as it currently has the highest carry in the fixed income universe. Meanwhile, we are underweight government bonds, with a preference for European peripheral bonds.

We are overweight commodities.

Because financial markets remain to some extent vulnerable to the virus and its variants, we are keeping hedges – which include derivative strategies, gold and the JPY – against disappointment in vaccination efficacy.

Our longer term-core convictions include (1) topics impacted by the need for sustainability, (2) resilient countries (via their domestic shares or index: China A- shares, German Dax) and (3) resilient sectors ( global technology, healthcare).