The activity cycle remains firmly in ‘downturn’ mode, with every country in the G10 region now in either ‘downturn’ or ‘recession’ territory. Macroeconomic data from the US have declined in recent months, as indicated by clearly weakening forward indicators, confirming the signal provided by our in-house models (since the beginning of the year) that the probability of recession was on the rise. In the euro zone, the business cycle has also taken a sharp hit and the probability of downturn has risen quite significantly, while in the UK the economy is still in a recessionary phase. The inflation cycle has also taken a downwards turn. The US inflation cycle has dipped below average into disinflation territory and, more importantly, the euro zone, at its peak in recent months, appears to have turned a corner, also declining somewhat. The debt cycle has dipped slightly (into negative territory), taking our framework from “deleveraging” to “repair”. This is indicative of a relatively weaker scenario, as nearly all countries have posted less supportive credit conditions. Unsurprisingly, in these conditions, central banks across the globe have continued to maintain their dovish stance, to the delight of investors, particularly in the US, where markets are already pricing in additional rate cuts before year-end. The ECB has already delivered a QE programme along with a rate cut. Monetary easing is also being driven by emerging markets, with the PBOC appearing ready to play its part in supporting the Chinese economy. Finally, some EM countries (India, Indonesia) have already implemented rate cuts in recent months, with more likely to follow.

Overall, the combination of lower growth, weaker business cycle, softer inflation and extremely supportive central banks is positive for Fixed Income markets and spread products in particular. However, after six months of falling rates (with an acceleration to the downside and tightening spreads), valuations are looking less appealing and the markets seem ready to take a breather following the rally. Furthermore, event risks have not subsided, with continued anxiety over Brexit in the UK, trade wars on several fronts and geopolitical risks such as the tensions between the US and Iran. Even so, in such a context, all eyes are focused on the world’s central banks, which are seen as the main drivers of markets. The fact that most of these banks have turned sharply dovish over 2019 has been the reason for the huge rally in bond markets, while at the same time the possibility of monetary policy disappointing in the future is also a source of investor concern. In the US, the debate is over the extent of the Fed rate cut (25 or 50 bps), and in Europe it is about the effectiveness of QE and how much ammunition is left in the tank. However, these distractions (regarding event risks, central banks and bets on a probable recession) should not deviate our attention from the fact that, on the whole, disinflation appears to have settled and weaker growth is here to stay. It is hard to ignore that business investment has certainly retreated and that this current expansion cycle has not closed the output gap during a period that has seen inflation peak. Now that the output gap is set to widen, in the context of an economic slowdown, disinflationary pressures are likely to be omnipresent, thereby fuelling further central bank assistance. The overall outlook is hence positive for bonds, though there are likely to be periods when markets take a breather (such as the present context), pullbacks are witnessed and some tactical profit-taking is carried out.

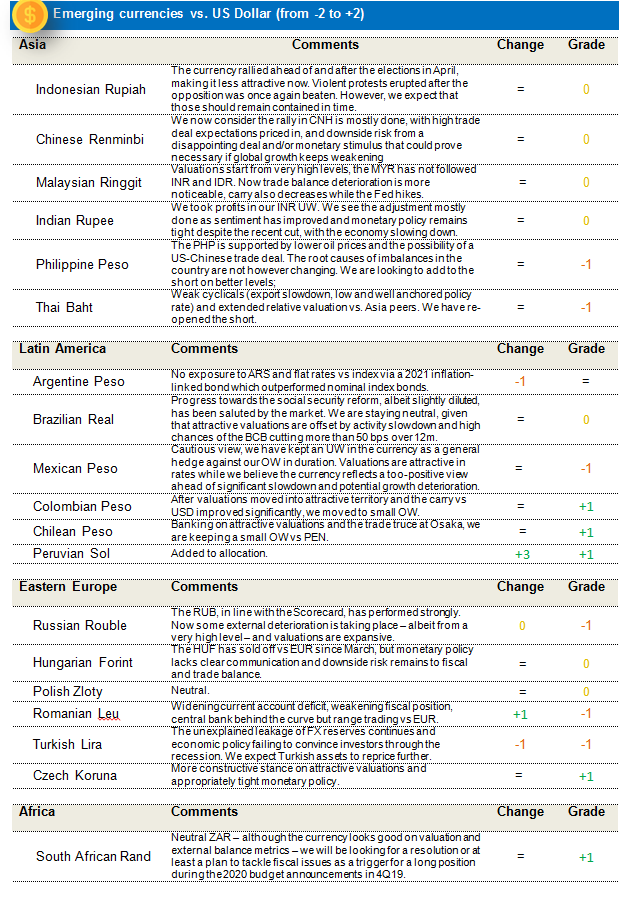

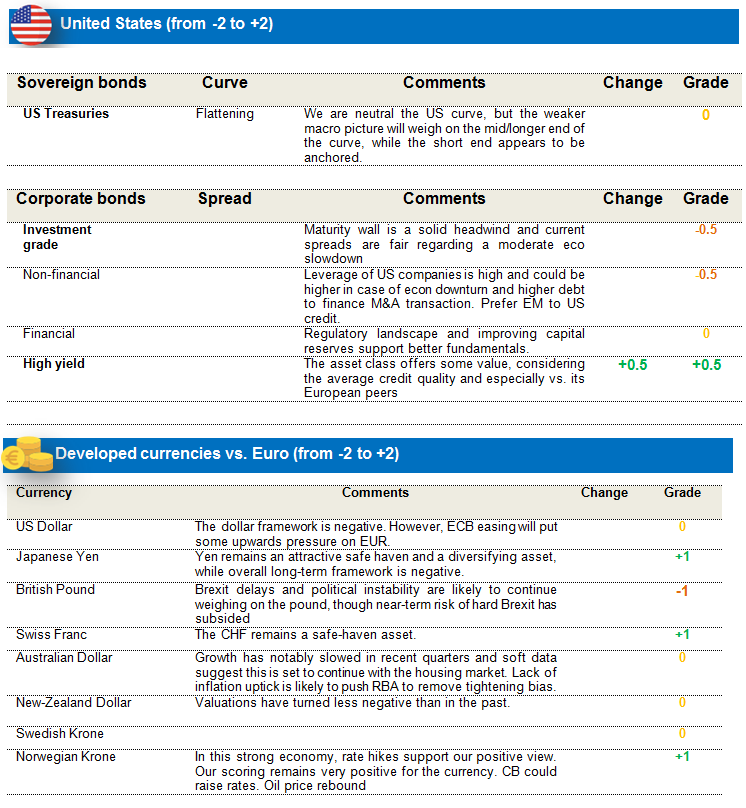

Neutral on US and tactically underweight core eurozone rates

The Fed continues to maintain a patient and flexible approach, while pointing tow downside risks in the global economy. With macro-economic data deteriorating and forward indicators falling short of expectations, it is increasingly likely that Jerome Powell, who is under pressure from President Trump, will announce a rate cut in the third quarter of 2019.We believe that the weak macroeconomic picture will continue to put pressure on the longer end of the US yield curve. However, following the sharp rally that has taken place since the beginning of the year and that saw US yields decline by half, the market is likely to take some profit. In this context, and as we await on central banks delivering on their promises, we have adopted a neutral stance towards US rates. The ECB has delivered on its promises by: announcing a package of measures that includes a cut of the deposit rate to -0.5% and a 2- tier system; extending forward guidance; restarting the quantitative easing program; and, finally, lengthening TLTRO maturities to 3 years. Furthermore, economic data in the euro zone remain fairly weak, despite some improvement in August, while inflation also fell considerably. Given the tight valuation, more challenging investor positioning and flow dynamics, we have set up a small duration underweight via options. This is a tactical protection, as we think that, with current challenging global economic, political and trade dynamics and the move by central banks towards easier monetary policies, the upturn in German rates should remain contained.

Positive view on Spain and Portugal, tactically long Italy

Non-core markets have continued to receive support from the ECB’s monetary policy. At the September meeting, Mario Draghi formally announced the return of QE, to the tune of 20 billion’s worth of bond-buying a month. He also insisted on the need to maintain an accommodative monetary policy for a prolonged period of time, with the evolution of the policy path linked to the evolution of inflation under rather stringent conditions. Flow dynamics linked to new purchases and reinvestments should continue to underpin non-core markets, compressing risk premium despite dissensions within the governing council about QE. Furthermore, the political risk that had weighed on Italy in recent months has retreated, with the 5-star movement able to agree to an alliance with PD (a more mainstream party), resulting in a less Euro-sceptical government and more market-friendly economic plans – a major hurdle in the past. Taking into account recent considerations that include the retracement of the tussle between the European Commission and the Italian government over the deficit, we feel that the rally in Italian rates might still have some legs. In this context, we prefer to tactically hold a positive stance towards Italy in our sovereign funds.

Developed Market Currencies: Neutral position on USD

The twin deficits exhibited by the US should keep the greenback under pressure vs. major currencies. Should the macroeconomic data continue to weaken, and the Fed cut its rates and adopt an outright dovish stance, the US dollar is likely to decline. However, with other CBs, including the ECB, also aggressively easing their monetary policies, currencies like the Euro are likely to see short-term declines vs the USD. In this context, we prefer to have a neutral position on the greenback and continue to tactically manage the position.

Our scoring remains positive on the Norwegian Krone and we have therefore maintained our long position on the currency, which is also supported by a relatively strong economy, where the business cycle – though in downturn territory – is unlikely to fall into recession and economic surprises should be positive. Finally, if the central bank continues hiking, this would boost the currency further.

Rate differentials remain detrimental and our long-term view also points to a decline in the overall score for the Yen. However, in the current environment marked by geopolitical uncertainty and a heavy dose of event risk, the Yen remains an attractive safe haven and a diversification tool. We therefore continue to manage the currency tactically, with a neutral stance at present.

Credit: Increase exposure to European Investment Grade

We maintain our favourable view on the European credit investment grade asset class, though we continue to monitor the situation in the context of a weaker European economy and rising idiosyncratic risk. Company fundamentals are not deteriorating as expected, as they are pursuing deleveraging and maintaining good operating margins. The credit quality on High Grade names appears healthy, with more upgrades than downgrades, unlike High Yield. European credit seems to be the only opportunity in a context of negative-yield sovereign bonds and therefore has enjoyed strong inflows. In the current context of the economic slowdown and the uncertainties regarding trade wars, Brexit and other geo-political risks, the ECB has decided to adopt an accommodative stance, cut rates and restart QE, all of which will have a positive impact on Investment Grade corporate bonds. With the current purchase programme, net supply will be negative, supporting the corporate bond cash market and containing any widening in spreads, which further reinforces the case for Eur. IG credit.

US High Yield and Emerging High Quality Credits offer interesting opportunities

We have a preference for US High Yield to European High Yield. At 450 bps, the asset class offers some value considering the average credit quality, and especially vs. its European peers. While the US recession is not currently our central scenario, US GDP growth is decelerating slightly under 2% for next year though financial conditions remain supportive and the Federal Reserve has promised to do more to sustain the current economic cycle. The European economy is more fragile, and the high-yield market more limited, as BB bonds have already reached their tightest level over the last 12 months and profit warnings are rising in the lower credit quality profile. So, selectivity is key as dispersion is rising and downgrade activity outpacing upgrades, with some sectors facing structural challenges and the default rate expected to continue to modestly rise towards 3.5% in the next 6 months.

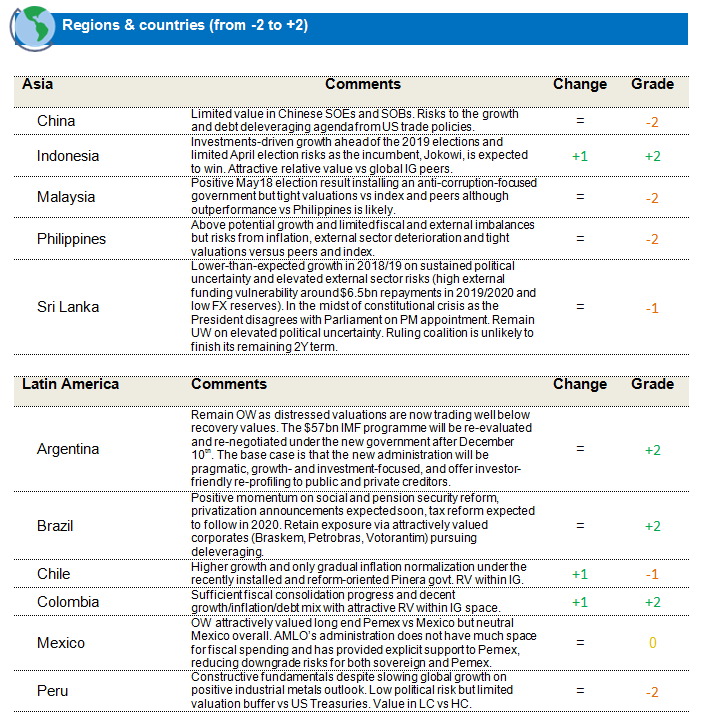

Emerging Markets: Moderately constructive

We remain cautiously constructive on EMD HC as the asset class continues to explicitly benefit from the aggressively dovish Fed and ECB stance and from the stable outlook for commodities, despite the unpredictability of the US-China trade relationship and unlikelihood od it being resolved in the near term. The imposition of EU trade tariffs in the autumn and Brexit also pose clear risks to the extension of the risky-asset rally. Absolute asset class valuations are not as attractive as at the start of the year, although there are pockets of value in selected EM credits, especially in B- and BB-rated credits, where we are concentrating exposures, and in relative terms – versus US credit – as the percentage of negative-yielding fixed income securities has increased beyond their 2016 highs (30% of the Bloomberg Global Aggregate index is now negative-yielding, with 90% yielding less than 3%).

In EMD LC, we are keeping our positive duration stance, on the premise that the easing signalled by the Fed and ECB will provide space for EM central banks to cut more than anticipated. We also added to lower-yielding local markets, favouring China as a hedge against trade-war escalation and global recession risk.

Our baseline scenario for 2019 is a weak but stabilizing EM and DM growth, which favours duration over EMFX. Within EMFX, we favour the currencies of countries that took advantage of the growth slowdown to compress internal demand and improve their external balances.

Hard currency

With a yield of 5.2%, EMD HC valuations are less compelling in absolute terms than at the end of 2018, and as EM risk premiums have already largely priced in a US-China trade tension de-escalation but still offer value in relative terms to a growing universe of negative-yielding global FI (at 30% by the end of August). The EM HY-to-IG spread is still attractive, as are the EM single and double-B rating categories versus their US HY counterparts. The medium-term case for EMD remains supported by the benign US Treasury and commodities outlook. Global growth and trade stabilization could support the next leg of EM spread compression but global data continue to soften and trade-war risks persist. On a one-year horizon, we expect EMD HC to return around 6%, on an assumption of 10Y US Treasury yields at 1.5% and EM spreads at 350bps.

We retain an overweight in HY versus IG, although we have scaled down that position materially since the end of July by additions to IG-rated Chile, Colombia, Indonesia, Panama and Romania, and reduced exposure to energy exporters like Bahrain, Nigeria and Oman.

In the HY space, we remain exposed to idiosyncratic stories like Egypt, Ghana and Ukraine as these continue to offer value relative to the balance of risks, and to attractively priced energy exporters like Angola, Bahrain and Ecuador. We retain exposure to Argentina as the bonds have already declined more than 45% over the month and are now trading below expected recovery values of around 60-70 cents on the US Dollar. In the IG space, we now hold large positions in Qatar, Colombia, Indonesia, Panama and Romania but remain underexposed to the most expensive parts of the IG universe like China, Malaysia, the Philippines and Peru.

We retain underweights in Lebanon, Russia and Saudi Arabia as we feel we are not adequately compensated for sanctions or political risks in these credits. In Brazil, Mexico and Turkey, we hold overweights in attractively priced quasi-sovereigns and corporate bonds versus underweights in sovereign bonds. We also retain a tactical 15% CDX.EM asset class protection position on elevated trade-war risks.

Local currency

We believe that, with a yield of 5.7%, EMD LC compares well to FI alternatives, especially as we are now expecting a respite from US-China trade tensions and US growth exceptionalism and in an environment of broad-based global monetary policy accommodation. On a one-year horizon, we expect EMD LC to return around 5.7%, assuming a conservative -1% EMFX and +1% duration returns. EMFX are unlikely to outperform in a global growth slowdown, although external rebalancing is taking place in most EMs and EM central banks have managed to deliver hiking cycles to maintain attractive FI risk premiums versus DM in 2018 that have not been unwound.

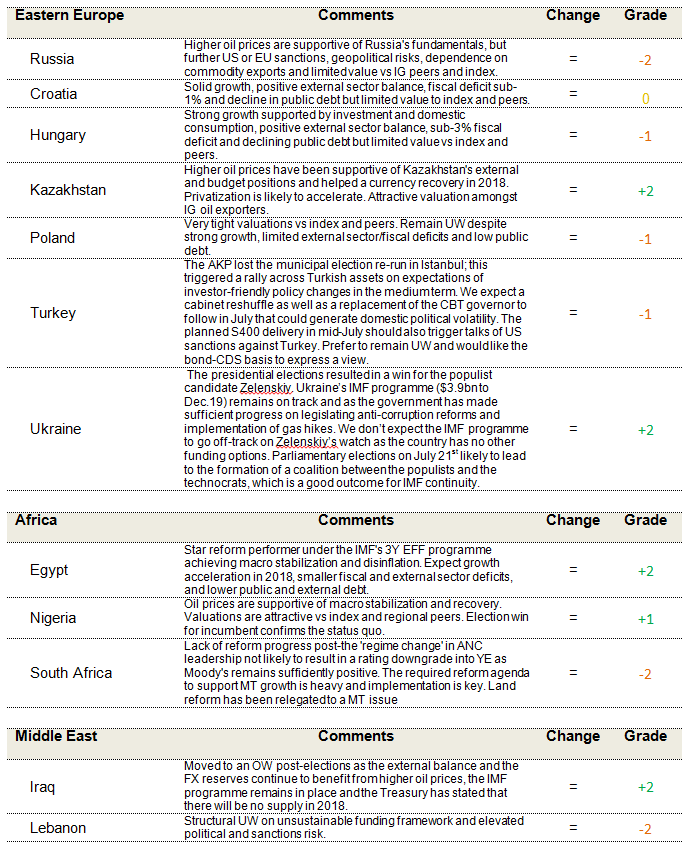

In EMD LC, we prefer to retain exposure to EM rates versus EM currencies and prefer bond markets that offer high-risk premiums versus US Treasuries, which happen to be represented by a wide range of low-yielding and high-yielding local markets. The EMD LC strategy is very long duration in low-yielders like China, Czech Republic, Malaysia and Poland, and high yielders like Indonesia, Mexico and South Africa; moderately long duration in high-yielders like Brazil, Peru, Russia and the Dominican Republic, and close to flat the rest of the EMD LC local bond markets.

The LC strategy is short EMFX overall (long USD position of 7.5%) and only holds small currency positions in frontier markets like the Dominican Republic Peso (DOP), Kazakhstan Tenge (KZT) and Ukrainian Hryvnia (UAH), where we also like local bonds. The LC strategy is short Latin America FX such as the Colombian Peso (COP), Mexican Peso (MXN), Peruvian Sol (PEN) and Asian FX such as the Chinese Yuan (CNH), Indonesian Rupiah (IDR), Indian Rupee (INR), Philippine Peso (PHP), and Thai Baht (THB), and flat CEEMEA FX with the exception of the Ruble (RUB). We are less positive on EMFX given the global slowdown and EMFX’s growth sensitivity, as well as the strong positive US Dollar momentum in negative global market environments.

In terms of preference, we prefer LC Rates followed by HC sovereign credit (especially the IG or UST-sensitive parts of the universe), and are negative EMFX.