The downturn in the activity cycle continued right up until year-end, with every country in the G10 region now in either ‘downturn’ or ‘recession’ territory. This trend has been perfectly in line with the recent IMF forecast which downgraded global growth. The US is certainly a participant in the trend and recent data prints such as the ISM manufacturing have seen decline, though the risk of recession appears to have receded. While markets point towards an un-inverted yield curve, the Feds intervention on repo markets could also be a reason for the phenomenon. In the euro zone, the business cycle continues to decelerate and the probability of downturn is now above 50%, while in Japan, the cycle is grinding lower The UK economy doesn’t appear to be improving and is still in a recessionary phase though uncertainty over Brexit has cleared up with a new date set by both sides (31st January 2020). All-in-all, the weakness in the global activity cycle, confirmed by our in-house models (since the beginning of the 2019), is present though the probability of an all-out recession has receded. Some good news, such as the signing of “phase one” in the US-China trade war and the containment of US-Iran tensions, has also led to better risk sentiment. In spite of historic efforts of central banks, inflation levels still remain stubbornly low.

However, we might observe a pause in central bank activity as some of them have started to indicate to potential revisions of their inflation targets. The Fed appears to be in a “wait-and-see mode” while the ECB (which has seen Christine Lagarde taking over the reins) launched a comprehensive review of its monetary policy targets and tools, that will end in June 2020. In spite of this, accommodation still continues to be present as G4 balance sheets are expanding as the Fed is now buying the very short end of the curve, accompanying the ECB and BoJ QE programs. EM countries (China, Brazil, India, …) are also on the dovish path with rate cuts and accommodation being very much present in their monetary policies.

Tactical underweight on Core European Rates, Neutral on US

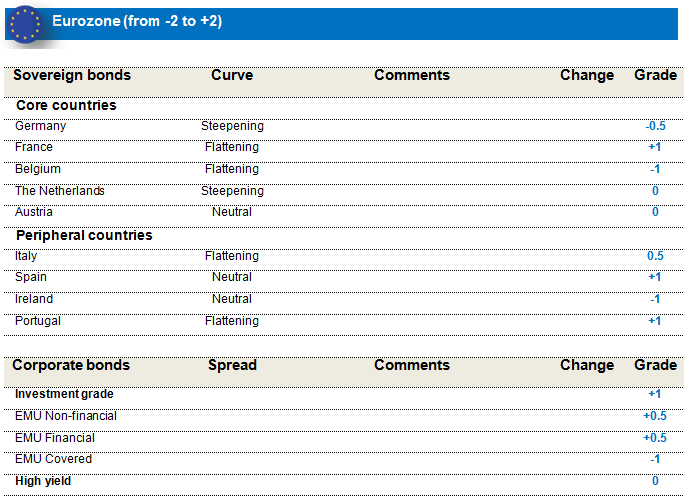

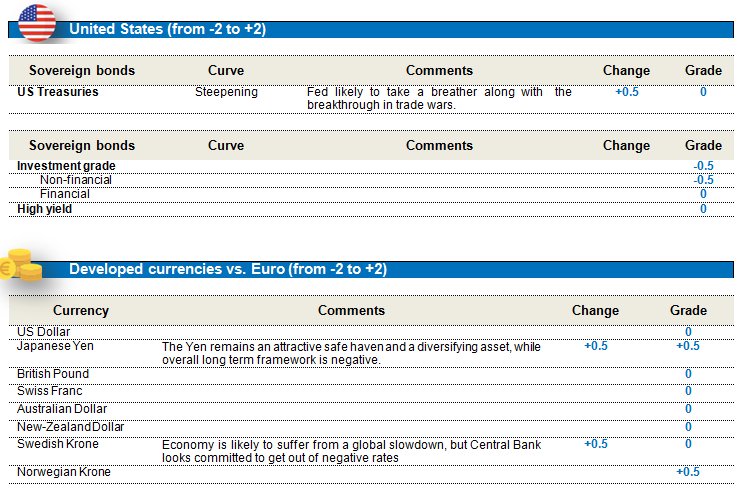

The biggest news over the recent weeks was the run-up to and the ultimate signing of the “phase 1” of the trade deal between the US and China. The reversion of the previously inverted US yield curve has added more positivity in markets, as it indicates lower probability of recession. If macro-economic data continues to stabilize, the Fed could maintain rates at current levels. The recent IMF forecast and macro-economic prints do call for some caution, and the Fed is under pressure to maintain a dovish stance during an election year where president Trump will demand an accommodative stance at worst. In this context, we prefer to move to a neutral stance on US rates rather than our previous negative stance. Core euro zone rates have seen a significant move upwards with German rates moving from -0.7 to -0.2 in a matter of 4 months, in the absence on growth or inflation moves. Indeed, it seems abating external risks (hard Brexit and Boris Johnson’s election, and “phase-one” success) has been enough to push core rates upwards. The move has also been helped to a certain extent by the news that the ECB board is divided in its appreciation of QE and that a review is being conduct on the efficiency of the program. While valuations could warrant some profit-taking after a strong move, we feel that in the current context, the rally in core yields could have some legs. We thus feel comfortable with a short position on German rates and we monitor the position in a very careful manner. The linkers market has delivered mixed performance as US and EUR markets performed well, while the UK was a laggard on the back of the strong rally of the Pound Sterling. We hold a slightly positive view on Euro linkers, which should benefit from ECB easing, attractive valuations as well as better supply dynamics.

Positive on Peripheral Sovereigns

Non-core markets have continued to benefit from the ECB’s quantitative easing. Flow dynamics linked to new purchases and reinvestments should continue to underpin non-core markets, especially since the ECB has not bought enough peripherals to satisfy the capital key targets.

Developed Market Currencies: Neutral USD

Our proprietary framework continues to point towards a negative view on the US dollar. The Fed’s rate cuts and dovish stance also point to a weaker dollar, with the US president clearly indicating his preference for a weaker greenback. However, we do expect that, after recent actions, central banks are going to take a breather. In this context, we prefer to have a neutral position on the greenback and we continue to tactically manage the position.

Credit: Maintain exposure to European Investment Grade

We We maintain our favourable view on the European credit investment grade asset class, we continue to closely monitor idiosyncratic risks. In the Euro IG portion, Credit quality on High Grade names appears healthy, with more upgrades than downgrades.

Emerging Markets: More constructive on expectation of global growth stabilization and recovery on trade war risks

We remain cautiously constructive on EMD HC as the asset class continues to explicitly benefit from the accommodative Developed Market and Emerging Market central bank stance, from the stable outlook for commodities and expectations of a near-term de-escalation of the US-China trade relationship. The likelihood of the US and China agreeing on a mini-Phase 1 trade deal by end of Q1 2020 at the latest should deliver an uptick in risk sentiment. Absolute asset class valuations are not as attractive as at the start of the year, although there are pockets of value in select EM credits, especially in B- and BB-rated credits, where we are concentrating exposures, and in relative terms – versus US credit – as the percentage of negative-yielding fixed income securities has increased beyond their 2016 highs.

In EMD LC, we are maintaining a small positive duration stance, in recognition of some residual relative value between EM and DM local bonds, although we scaled down our duration exposure during the 4th quarter, as Emerging Market central banks were more than half-way through their easing cycles.

Our baseline scenario for 2020 is for but stabilizing EM and DM growth which favors EMFX over duration. Within EMFX we favour the currencies of countries that took advantage of the growth slowdown to compress internal demand and improve their external balances.

Hard currency

EMD HC rallied sharply post the announcement of a US-China trade deal, in line with other risky assets like US Equities and EMFX In a classical 'risk-on' market, Treasury and Spread returns diverged. EM spreads tightened by 34bps (to 291 bps) and 10Y US Treasury yields rose by 14 bps (to 1.92%).

The newly formed Argentine cabinet was quick to implement a host of crisis fighting measures - tax hikes, more conservative than expected emergency fiscal bill, extension of FX T-bill payments till Aug-20 - all pointing towards a version of more pragmatic than expected, growth biased Peronist stance. HY (3.6%) out-performed IG (0.7%) with Argentina (+21.6%) and Ecuador (15.3%) posting the highest and Suriname (-2.1%) and Tajikistan (-0.3%) the lowest returns.

With a yield of 4.9%, EMD HC valuations are less compelling in absolute terms than at the start of 2019, although they still offer value, in relative terms, to a still-large universe of negative-yielding global FI (at 20% by the end of December). The EM HY to IG spread is still attractive as are the EM single and double B rating categories versus their US HY counterparts. The medium term case for EMD remains supported by the stable US Treasuries and Commodities outlook. Global growth and trade stabilization can support the next leg of EM spread compression in environment of low trade tensions. On a one year horizon, we expect EMD HC to return around 3.25%, on an assumption of 10Y US Treasury yields at 1.75% and EM spreads at 325bps.

We retain an overweight of HY versus IG.

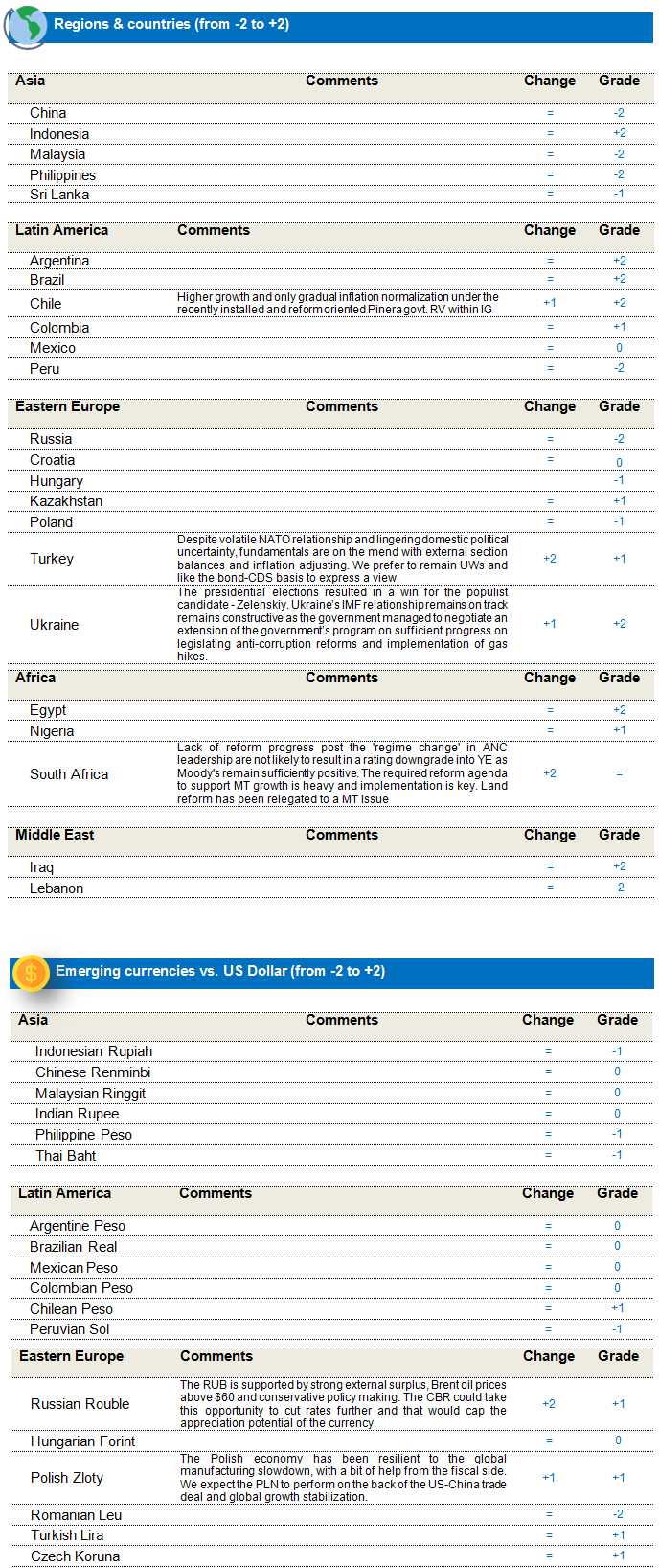

In the HY space, we remain exposed to idiosyncratic stories like Egypt, Ghana and Ukraine, as these continue to offer value relative to the balance of risks, and to attractively priced energy exporters like Angola, Bahrain and Ecuador. We retain exposure to Argentina, as assets are trading as “distressed” (around the 40s) and well below expected recovery values of around 60-70 cents on the US Dollar. In the IG space, we hold positions in Indonesia and Romania but remain underexposed to the most expensive parts of the IG universe like China, Malaysia, the Philippines and Peru.

We have retained underweights in Lebanon, Russia and Saudi Arabia, as we feel we are not being compensated for sanctions or political risks in these credits. In Brazil, Mexico and Turkey, we hold overweights in attractively priced quasi-sovereigns and corporate bonds versus underweights in sovereign bonds. We also retain a tactical 6% CDX.EM asset class protection position on elevated trade war risks.

Local currency

EMD LC returned 4.1% in December, mostly from FX (3.1%), with duration and carry contributing 0.5% each. Against a positive backdrop featuring the US-China “phase 1” trade deal and a tentative bottoming out of the global economy, risky assets rallied, the US curve bear steepened and local currency debt performed strongly, catching up after November's correction. Latin American FX outperformed, led by the COP (7.4%), CLP (7.3%) and BRL (5%). CEE FX outperformed the EUR, supported by a resilient macro and central banks on hold. Turkey underperformed amid profit taking and the nationalistic noise from Erdogan. EM rates tightened 20 bps against UST. Mexico outperformed (-19 bps) supported by lower inflation and moderate slowdown, with the fiscal remaining sound. Colombia and Chile retrace previous losses (-15 bps each), as well as South Africa (-16 bps) supported by a slowing economy.

We believe that with a yield of 5.2%, compares well to FI alternatives EMD LC compares well to FI alternatives especially given the respite from US-China trade tensions and global growth showing signs of picking up. The medium term case for EMD also remains supported by the improvement in the quality of fundamentals, benign inflation outlook and accommodative monetary policy globally.

In EMD LC, we took profits in our lower yielding LC duration exposure and are now more exposed to higher yielding LC markets after the December announcement of a US-China trade deal raised hopes for global growth stabilization and as value in lower yielding, Treasury sensitive EM markets seemed exhausted.

The EMD LC strategy is now only marginally long duration via high yielders like Indonesia, Mexico, South Africa. ; moderately long duration in high yielders like Peru and the Dominican Republic, and is close to flat the rest of the EMD LC local bond markets.