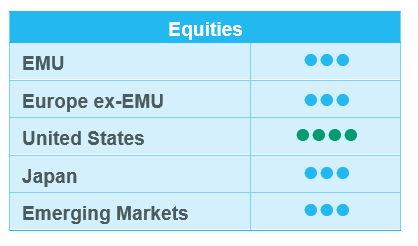

European equities: Europe outperforming the US

In January, European equities closed the month higher, outperforming the US and narrowing part of the valuation gap between the two sides of the Atlantic. In addition to attractive valuation multiples, the eurozone has benefited from improving macro data (the composite PMI edged into expansionary territory at 50.2 in January and retail sales have risen for five consecutive months) and the ongoing rate-cutting cycle from the European Central Bank (ECB), while the Fed has decided to pause rate cuts. The ECB cut its policy rate by 25 bps to 2.75% in January and still sees this level as restrictive, which suggests further rate cuts over the coming months.

No strong performance dispersion

Since the last Committee (14 January), European equities have performed well, with no strong performance dispersion between small/mid and large caps. Value stocks slightly outperformed Growth stocks, for both large and small/mid-caps.

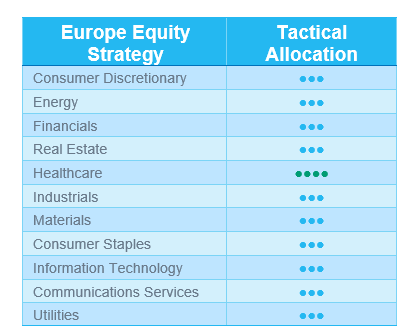

Cyclical sectors outperformed the broader market, with a strong performance across all sectors. The biggest outperformers were financials, real estate and consumer discretionary, followed by materials and industrials.

Defensive sectors also trended positively, especially healthcare, consumer staples and utilities, while performance was more limited for energy.

Lastly, communication services performed well, while information technology underperformed, given the negative performance of some names exposed to AI, which suffered following the launch of DeepSeek.

In terms of individual stocks, the main contributors since the last Committee were Spotify (+34%), SAP (+25%), Banco Santander (+18%) and EssilorLuxottica (+16%).

Earnings expectations & valuations

Fundamentals remain well oriented for European equities. Positive earnings revisions have been supportive for the European market. 12-month forward earnings growth now stands at 8.3%, up vs. the last Committee (7.7%).

Consensus expects this EPS growth to be driven by information technology, consumer discretionary, communication services, industrials, materials and healthcare (with double-digit EPS growth for each). Conversely, energy and utilities remain the only sectors dragging down expected earnings with negative growth.

European valuation multiples have slightly increased since the last Committee, with 12-month forward P/E of 14.0x (vs 13.3x previously), which remains well below US multiples (22.4x). Information technology and industrials are the most expensive sectors (P/E of 26.9x and 19.0x respectively) while energy and financials are the cheapest (P/E of 7.9x and 9.6x respectively).

No change in European grades

No change has been made in terms of sector grades.

We confirm our positive stance (+1) on healthcare, as the sector’s fundamentals remain well oriented and its US dollar exposure will be a tailwind.

We have a neutral grade on the other sectors. However, we are more constructive on European semiconductors (ASML, Infineon) and an upgrade could occur over the next few weeks at a good entry level, as this sector should benefit from the recovery in consumer electronics in H2 2025 and 2026.

US equities: A solid start to the year

US equity markets started the year on a strong note, bolstered by President Trump’s return to the White House, which fueled expectations of deregulation and tax cuts. While the emergence of Chinese artificial intelligence company DeepSeek briefly sparked volatility in the US technology sector, investor confidence remained resilient. Market participants continued to embrace the strength of the US economy and reaffirmed their belief in the country's leadership within the AI space.

Performance dispersion

US equities have performed well in recent weeks, maintaining their upward trend despite temporary volatility following the announcement made by Chinese AI company DeepSeek.

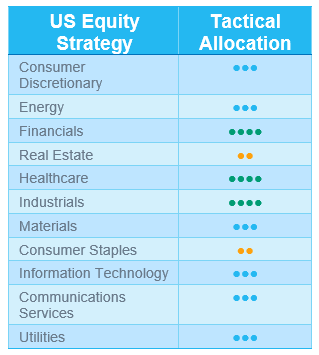

Sector performances varied significantly. Financials outperformed the broader market, driven by expectations of reduced regulation and excellent Q4 results, while consumer staples (especially distribution and retail, less impacted by potential tariffs and a stronger US dollar) also delivered attractive returns. Real estate and healthcare also performed well relative to the market.

On the downside, energy was the only sector to post negative returns, as Brent crude oil prices fell below $74 per barrel. Information technology underperformed, particularly large cap stocks and key AI beneficiaries, as investors reacted to DeepSeek’s ability to develop efficient, low-cost AI models. Consumer discretionary and industrials also lagged the broader market.

Ongoing Q4 2024 earnings season

Investors are currently focused on corporate earnings reports. As of writing, more than 60% of S&P 500 companies have released their actual results.

Of these, 77% have reported earnings per share exceeding expectations, resulting in a blended year-on-year earnings growth of 16.4%—the highest since Q4 2021. On average, companies are exceeding earnings estimates by 7.5%, according to FactSet’s Earnings Insight report.

Eight of the 11 sectors have posted earnings growth, with financials, communication services, technology and healthcare posting double-digit gains. Energy, however, remains the weakest sector, experiencing a double-digit earnings decline.

Looking ahead, earnings growth for the next 12 months is projected to near 14%, driven primarily by information technology, healthcare and industrials. In this context, the S&P 500's forward 12-month price-to-earnings ratio stands at 22—above both the 5-year and 10-year averages, but not excessively high.

Upgrade Healthcare

We maintained a consistent strategic approach to sector exposure, continuing to favour cyclical sectors such as industrials and financials.

- Industrials stand to benefit from ongoing reshoring trends, the prospect of tax cuts following Trump’s re-election and expectations of a stronger economy.

- Financials are well positioned to gain from looser regulations, increased M&A activity, higher long-term interest rates and potentially more shareholder-friendly initiatives, including dividend payouts and capital returns.

- However, we have upgraded our stance on healthcare, raising it to +1 from neutral, based on:

- A favourable earnings growth outlook, with 2025 estimates exceeding the market average across all regions and benefiting from a more favourable comparison base than sectors like IT.

- Attractive valuations, both compared to other sectors and to the sector’s own history.

- The sector has typically outperformed in the 12 months following US presidential elections.

- Limited impact from tariffs, which, while present, are expected to be less significant than in other sectors.

- One caveat though: there are still a lot of unknowns regarding healthcare policy under the Trump administration (drug pricing, developments regarding Medicare/Medicaid, Department of Health and Human Services organisation, etc.).

Emerging equities: Trailing developed markets

In January, MSCI EM index gained +1.7% (in USD), underperforming developed markets (3.5%). The month started on a positive note, with a weaker USD, improving sentiment in AI-driven tech stocks and resilient commodity prices. However, optimism faded towards the month-end, following the announcement of new US tariffs on Canada (25%), Mexico (25%), and China (10%). After negotiations, the introduction of tariffs on Canada and Mexico was paused.

Latin America staged a notable recovery (+9.4%), rebounding from last year’s macroeconomic volatility (Latam currencies also gained). Meanwhile, China’s AI sector saw a major boost with the release of DeepSeek, an advanced AI model that delivers top-tier global results while maintaining cost efficiency. This shifted investor preference toward AI application software over traditional hardware and data centre investments.

In commodities, Brent crude rose 2.8%, while gold (+6.6%) and silver (+10.3%) surged on safe-haven demand amid geopolitical uncertainties. US Treasury yields ended the month at 4.58%, retreating from mid-month highs. Taiwan benefited from robust demand in the semiconductor sector, driven by AI acceleration. In contrast, Korea faced political instability, hampering confidence in key industries like technology.

Outlook and drivers

As 2025 unfolds, geopolitics remain central to the dynamics of EM and beyond. The Trump administration has introduced new trade policy uncertainties. The markets will closely monitor upcoming trade negotiations, but the scope and impact of potential tariffs remain a wild card, especially for EM economies reliant on exports.

The Chinese market trended upwards, driven by expectations of further targeted stimulus. Policymakers face a critical moment in restoring social confidence, with key signals to watch, including property market support, credit easing and tech sector investments.

Thematically, AI continues to drive sectoral growth in emerging markets. The rise of DeepSeek highlights that AI investment opportunities in emerging markets are proving far more expansive than initially anticipated, extending beyond AI infrastructure into globally competitive AI software development.

Amid heightened market volatility, a reactive, selective and flexible investment approach is essential. The portfolio benefits from its strengths to dynamically calibrate risk exposure, capitalise on macroeconomic shifts and position itself in high-conviction structural themes over the long term.

POSITIONING UPDATE

Regions

Regional preference: China > India – China is recovering on improving macro fundamentals and positive market sentiment, while India is showing signs of peaking, leading to investor rotation into China.

China

- We have upgraded several sectors in China (see below), on the back of a strong outlook in e-commerce, EVs and media.

- Tariff concerns eased, proving less disruptive than expected, although volatility persists.

- DeepSeek’s success bolsters China’s tech sector, driving gains in software, cloud and chipmakers. The rally remains concentrated.

- Economic data showed an incremental improvement. The next policy meeting is scheduled for March. Multiple subjects will be on the agenda: to boost consumption, support real estate and stabilise foreign investment & equity markets.

India

The market peaked, with rich valuations, an unimpressive earnings season and a wave of IPOs. Investors are rotating into China. Modi-Trump meeting in Washington – a key event to monitor for potential policy shifts.

Sectors

Autos: We remain neutral on the back of a mixed outlook in India and Korea.

Chinese consumer discretionary: We have upgraded the sector given the global dominant position of several sub-sectors, such as e-commerce and EVs.

Chinese e-commerce: Alibaba is in negotiations with Apple to provide exclusive AI services in China. PDD has seen some geopolitical pressures ease, with Temu’s results proving resilient.

Chinese EVs: The China EV sector remains strong, led by BYD’s undisputed global leadership, Xiaomi’s continued expansion and Xpeng’s significant supply chain restructuring.

Chinese media: We have upgraded Chinese media. Tencent stands out as the country’s largest IT services company, serving over a billion users globally across social media, gaming and short videos. The company’s AI investments present additional long-term upside potential.

Precious metals, especially gold, are gaining momentum following central banks’ purchasing and global uncertainties.

Technology: We have become more selective. We adjusted our exposure with some rotation into China as new opportunities emerge.