We maintain an overweight stance on global equities, adopting a more balanced approach across sectors and regions. Notably, we have a renewed interest in Europe and China, as the catch-up trade in these regions still has potential upside: a range of macroeconomic, geopolitical and technological factors have introduced notable shifts that investors must carefully assess. The key question remains whether these changes are temporary fluctuations or structural transformations. Regardless, they are actively shaping market trends and investment strategies.

Regarding fixed income, we prefer duration exposure in core Europe (Germany) due to expectations of continued low growth and disinflation trends in 2025. Conversely, we are cautious on US duration, anticipating upside risks to US yields. Additionally, we remain long on the US dollar and Japanese yen.

Ukraine ceasefire talks: a potential geopolitical turning point

The Eurostoxx50 index recently achieved a new all-time closing high for the first time in 25 years, driven in part by optimism surrounding potential ceasefire talks between Ukraine and Russia. Markets view the prospect of peace as a positive catalyst for the Euro and European equities, particularly if easing sanctions reduces commodity costs. A successful resolution could stabilise the region, enhance global trade and improve investor confidence. Conversely, a failure could sustain inflationary pressures and geopolitical risk premiums.

From a geopolitical standpoint, Western Europe remains wary of Russia’s long-term intentions. Therefore, the greatest worry for Western Europe remains the Putin regime. However, European leaders must also navigate the challenges of post-war reconstruction and potential peacekeeping responsibilities, while facing limited influence in the negotiations due to the role of the US administration. To some extent, for Western European politicians, the second-biggest risk is the Trump administration. In this context, we adjusted our tactical positioning upwards without changing our mind regarding the long-term allocation.

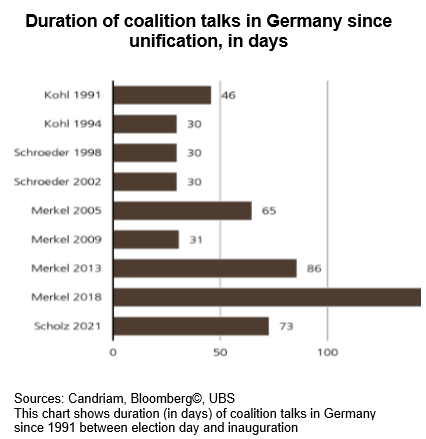

German elections and the potential of reform of the debt brake

Another key factor supporting our tactical upgrade of European equities during the past weeks has been the upcoming German general elections. The potential change in government could lead to discussions on reforming the “debt brake” – a constitutional limit on government borrowing. A CDU-led coalition with the SPD or the Green party could introduce fiscal flexibility, promoting public investment in infrastructure, digitalisation and green energy.

Any constitutional amendment, however, requires a two-thirds majority in parliament. Given that the far-right AfD and the conservative-left BSW currently poll between 25% and 28% collectively, they could block any changes if they surpass one-third of the vote. This is a risk to keep in mind for election night on 23 February.

Should Germany loosen its fiscal constraints, the broader EU economic outlook could improve, enhancing economic growth and stability in European financial markets. However, if coalition talks extend over months – as has increasingly been the case in recent elections – short-term market volatility may arise.

Tariff policy of the new US administration

Geopolitical tensions and trade policy unpredictability continue to pose risks to global market stability. The new US administration has reinstated and expanded tariffs on steel and aluminium imports, aiming to protect domestic industries. While this strategy seeks to bolster US manufacturing, it introduces uncertainty into global trade relations and may provoke retaliatory measures from affected nations. Rising bond yields, closely linked to the risk of inflationary measures via higher tariffs and lower immigration-linked labour market supply, constitute a risk to our constructive scenario on equities.

The tariff policies implemented by the new US administration could become a pivotal force and shake financial markets in the future. With an emphasis on reshoring industries, protecting domestic employment and addressing trade imbalances, these policies may affect global supply chains. Tariff adjustments, particularly with China and Europe, could contribute to volatility in equity, bond and currency markets.

Can a potential upcoming trade war turn into a currency war? It is too early to tell, but the impact of a weaker currency has undoubtedly been a support for European equities since the start of the year: profit expectations have evolved more favourably in recent weeks, supporting the outperformance so far in 2025. To sum up, Europe is benefiting from renewed investor interest. In this environment, since January we have rebalanced our regional allocation towards more Europe but remain flexible to adapt our allocation at any time.

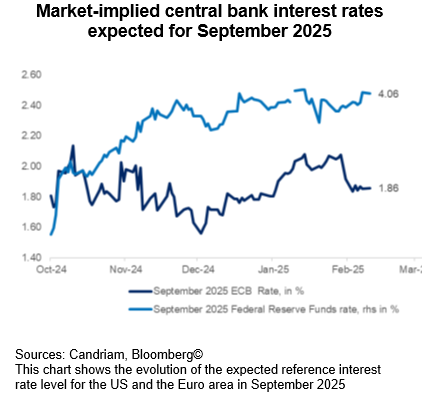

Monetary policy divergence between Fed, ECB and BoJ

While we have witnessed synchronised upward movements (in 2022/23) and downward movements (in 2024) in key reference rates, central banks’ reaction functions have started to take into account the aforementioned shifts. The divergence in monetary policies among the Federal Reserve (Fed), the European Central Bank (ECB), and the Bank of Japan (BoJ) is creating distinct economic conditions across regions, affecting global liquidity and capital flows. While the Fed remains in “wait-and-see” mode until inflation further decelerates, the ECB has adopted a more accommodative stance, balancing inflation control with economic stability. Markets currently anticipate a single cut in the Fed’s policy rate by the end of summer, while the ECB is expected to reduce rates by an additional 75 basis points.

Meanwhile, the BoJ has begun shifting away from its ultra-loose policy, providing some support to the Japanese yen. These divergent strategies will influence exchange rates, medium-term bond yields and investor positioning.

From an investment perspective, this divergence underscores the importance of selectivity in fixed-income markets. We maintain a slightly long duration stance in core European sovereign bonds (via German Bunds) while keeping a short duration position in the US. This exposure should work as a protection in a more adverse scenario if US 10-year sovereign bond yields rise above 5%. Based on this, we are slightly long on the US dollar and expect the Japanese yen to benefit from policy shifts and its safe-haven status.

We remain neutral on emerging market debt due to its vulnerability to higher US tariffs, despite attractive carry opportunities. In credit markets, we continue to hold a neutral allocation in both Investment Grade and High Yield, as spreads remain tight and default risk appears limited.

China’s DeepSeek innovation: a technological game changer

China’s introduction of DeepSeek, an advanced Artificial Intelligence (AI) model, showcases the country’s rapid technological advancements and its strategic focus on innovation. DeepSeek’s open-source approach and cost-efficiency have positioned it as a formidable competitor to Western AI models, highlighting the shifting dynamics in the global tech landscape.

Moreover, its impact extends globally, as AI-powered solutions reshape the competitive landscape, compelling firms worldwide to adapt or risk obsolescence. This development underscores China’s growing influence in the AI sector and its potential to reshape global technological leadership. Its future impact on markets could be substantial.

We have upgraded China to overweight last month (at the expense of India, which has been downgraded to neutral) and note that investor appetite toward the Chinese equity market has increased following the introduction of the DeepSeek model.

As we navigate 2025, maintaining a balanced and adaptable investment strategy will be essential amid ongoing macroeconomic, geopolitical and technological changes. Each factor, from trade policies and geopolitical negotiations to technological innovations and monetary policies, plays a crucial role in shaping the economic environment. Understanding and adapting rapidly to these changes is essential to seize the opportunities arising.