Investors had a few months to get mentally prepared for the return of Donald Trump to the White House. While he has not disappointed and started his second term with a bang, the real surprise came from China with the introduction of DeepSeek to the world. The results announced by this technology company had the effect of a financial quake towards some of the star market performers over the last quarters.

Despite the sharp selloff in the technology space, overall, equity market indices performed well during the month. European equities outperformed other regions returning high single-digit positive returns. Japanese, Indian and Chinese equities lagged most regions printing low single-digit negative figures. At a sector level, European technology, financials and consumer discretionary outperformed US technology and European utilities and consumer staples.

Sovereign yields for medium and longer term maturities in Europe and the United States widened 10 to 20 basis points to revert to same level at the end of the month. Corporate investment grade spreads remain tight and high yield spreads have tightened by another 10 to 20 basis points.

The HFRX Global Hedge Fund EUR returned +0.88% over the month.

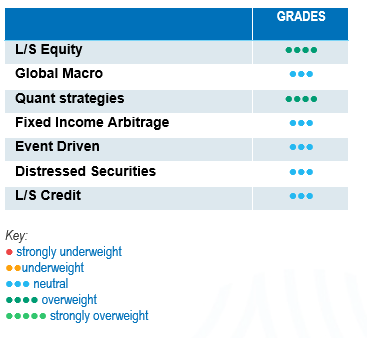

Long-Short Equity

Long-Short Equity strategies performed well during the month despite the volatility experienced by AI equity ecosystem. During the last week of January, strategies managed to limit the downside of the technology selloff and recover the losses by the end of the week. Although absolute performances were good, dispersion was also important. Strategies investing in Europe generated similar absolute returns to those focused on the US and Asia, but had a much lower upside capture ratio of European equities performance. On average, European managers did not buy into January’s equities rally. The Long-Short Equity universe is very rich in terms of opportunities and diversified in terms of styles. In a world of sustained uncertainty and of diverging economic performance, Long-Short Equity strategies are well-positioned to benefit from a broadening market opportunity set and increasing economic divergence.

Global Macro

On average, Global macro strategies generated low single-digit positive returns. Rates and currencies experienced some volatility during the month as markets moved on the announcement of tariffs by the Trump administration. Most of these moves reverted, as much of the tariff action failed to materialize for now. This is perhaps one of the biggest challenges for global macro managers presently; building and maintaining trading positions throughout the noise of this Administration’s communication style. We think that the economic decoupling across the major economic regional powerhouses will offer interesting investment opportunities for Global Macro managers. However, good risk management capabilities will be important to navigate the expected higher volatility swings.

Quant strategies

Quantitative strategies performed well during the month. Trend-following models generated positive return driving contributions from trading positions in currencies and commodities. Multi-Strategy Quantitative programs also performed well during the month. Systematic strategies continue to add value to portfolios with strong performance generation and providing diversification to traditional asset classes.

Fixed Income Arbitrage

After months of uncertainty surrounding inflation persistence and economic strength, central banks have adopted a more dovish stance, acknowledging the need for rate cuts as inflation normalizes downward. Since the beginning of the year, economic data has pointed to growing uncertainty regarding inflation and economic growth across developed markets, with significant regional divergences. In the US, mixed macroeconomic data, combined with the potential impacts of Trump’s measures, have halted the steepening of the yield curve. In Europe and the UK, the 2-10 year spreads have remained unchanged, highlighting how market dynamics are increasingly uncorrelated across regions. In Japan, the end of ultra-loose monetary policy presents both relative value (RV) and directional opportunities. This environment has been highly supportive for the fixed-income space, both in terms of relative value and directional strategies.

Risk arbitrage – Event-driven

Event-Driven strategies performed well during the month with allocations to Merger Arbitrage and Special Situations both contributing positively to returns. The opportunity set for Merger Arbitrage during 2025 is expected to improve with a much more business-friendly Administration. However, deal selection will remain an important focus of attention. The confrontational style of the new US president might be a source of concern for cross-border deals. Another source of concern for increasing the number of deals announced is the stability of the interest rate trajectory.

Distressed

Default rates have started to tick upwards recently but, overall, defaults remain concentrated in specific sectors. Most corporations were able to refinance opportunistically their outstanding debt at lower rates during the 2020-2021 period. Distressed specialists remain focused on idiosyncratic opportunities, remain cautious about high yield issues as spreads are close to all-time lows and have identified cracks in specific areas of the loan market. Stressed debt strategies were able to source interesting opportunities in balance sheet restructuring and liquidity provision to specific market participants.

Long short credit

Base interest rates remain wide offering to investors in credit decent yields. However, corporate spreads are close to all-time lows. We wonder if investors are being appropriately remunerated for the risk taken. Managers have concentrated their portfolio into their highest fundamental convictions, increased the level of hedges and lowered strategy directionality. On the other side, such a rich market generates numerous opportunities for alpha shorts. Although rates are initiating a cut cycle, they remain at high levels which favours alpha generation both on long and short positions as fundamental research becomes more important in portfolio construction. Absolute return or hedged investment approaches have gained more relevance with the increase of idiosyncratic risks and geopolitical uncertainty. Risk diversification is important and should be an integral part of the investment allocation process.